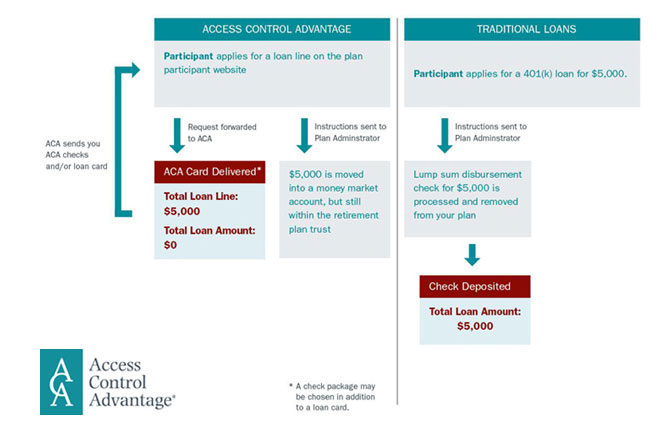

Participants apply for revolving loan lines through ACA the same way they would for lump sum loans. Once approved, instead of the custodian issuing a check to the participant (money leaving the plan), ACA moves the participant's requested loan amount to an interest-bearing cash account held within the plan. This becomes the participant's revolving loan line. ACA provides the participant with checks and/or an ACA debit card to draw upon funds from the revolving loan line. The unique advantage with ACA is that until the participant accesses money held within the revolving loan line, the participant doesn't actually incur a loan or loan repayment obligation. With ACA, the participant's requested loan amount stays in the plan until the exact moment the money is needed and in the exact amount needed.

Illustrating the difference

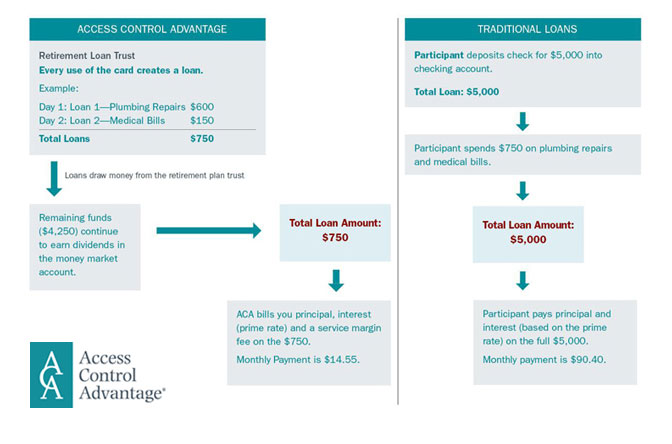

Assume that Joe, a participant in the plan, requests a lump sum loan for $5,000. Upon receipt of his check for $5,000, he deposits it into his checking account. He then immediately pays off a medical bill for $150 and pays an emergency plumbing bill for $600.

- Total spent = $750

- Total loan = $5,000

- The remaining $4,250 from the loan is comingled with Joe's other personal funds and is highly likely to be spent.

- Total spent = $750

- Total loan = $750

- Total loan assets remaining in the plan and still growing tax-deferred = $4,250

- Joe still has access to the remaining $4,250 in the ACA revolving loan line. However, if his financial need passes, he can re–direct any portion of his remaining revolving loan line balance back to his "core" funds at any time.

| Click on the images below to view illustrations | ||

|

|

|

The Power of ACA

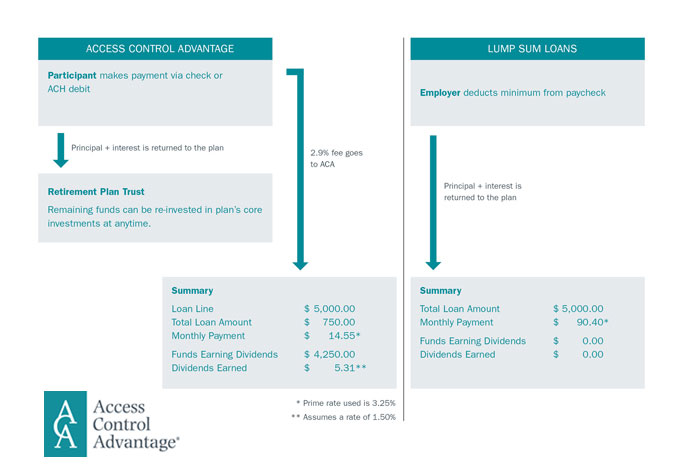

The aggregate of a participant's transactions for each day is treated as an individual loan with its own amortization schedule. Any amount not used remains in the plan until it is expended or returned to the core investments. With the unique concept of establishing a revolving loan line when a participant requests a loan, ACA empowers the participant to borrow the exact amount needed at the exact time needed. This eliminates excess borrowing that results from "grossing up" a loan request. And eliminating excess borrowing significantly reduces the plan asset leakage while providing the participant a smart way to access their funds. More assets remain in the plan–better for the participant and better for the recordkeeper too. (Note: ACA's statistical experience shows that, on average, 30% of the original revolving loan line balance remains in the plan and is never spent. That's 30% more assets retained under management versus current lump sum loan programs.)